Shirley K Data

Deep Learning Project

This python project explores Lending Club data to predict whether a person will pay off their loan. The data was cleaned and engineered for use with a neural network model.

Library and Data Imports

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

%matplotlib inlinedf = pd.read_csv('../DATA/lending_club_loan_two.csv')df.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 396030 entries, 0 to 396029

Data columns (total 27 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 loan_amnt 396030 non-null float64

1 term 396030 non-null object

2 int_rate 396030 non-null float64

3 installment 396030 non-null float64

4 grade 396030 non-null object

5 sub_grade 396030 non-null object

6 emp_title 373103 non-null object

7 emp_length 377729 non-null object

8 home_ownership 396030 non-null object

9 annual_inc 396030 non-null float64

10 verification_status 396030 non-null object

11 issue_d 396030 non-null object

12 loan_status 396030 non-null object

13 purpose 396030 non-null object

14 title 394275 non-null object

15 dti 396030 non-null float64

16 earliest_cr_line 396030 non-null object

17 open_acc 396030 non-null float64

18 pub_rec 396030 non-null float64

19 revol_bal 396030 non-null float64

20 revol_util 395754 non-null float64

21 total_acc 396030 non-null float64

22 initial_list_status 396030 non-null object

23 application_type 396030 non-null object

24 mort_acc 358235 non-null float64

25 pub_rec_bankruptcies 395495 non-null float64

26 address 396030 non-null object

dtypes: float64(12), object(15)

memory usage: 81.6+ MBExploratory Data Analysis

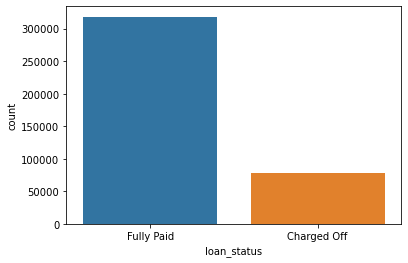

The following countplot shows the target variable distribution.

Ideally, the distribution would be more even.

sns.countplot(x='loan_status',data=df)<AxesSubplot:xlabel='loan_status', ylabel='count'>

The following histogram shows the number of loans for each dollar amount.

There are noticeable peaks at each 5000th increments.

plt.figure(figsize=(12,8))

sns.histplot(df['loan_amnt'],bins=40)<AxesSubplot:xlabel='loan_amnt', ylabel='Count'>

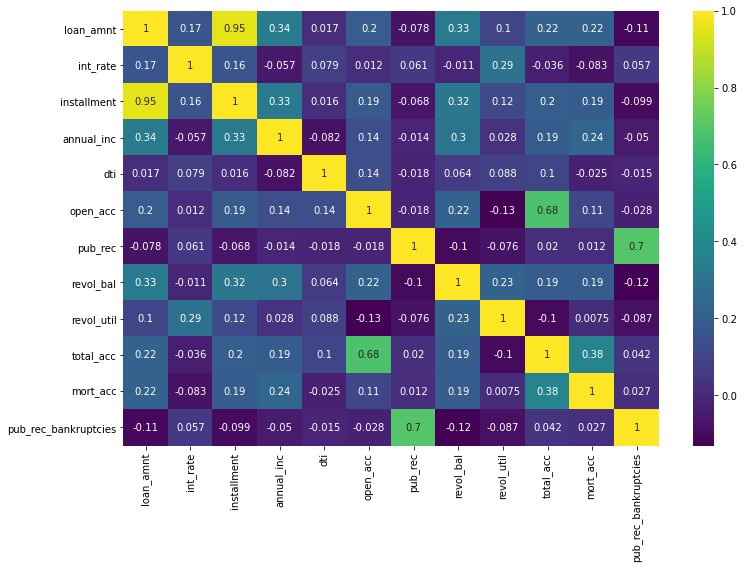

df.corr()| loan_amnt | int_rate | installment | annual_inc | dti | open_acc | pub_rec | revol_bal | revol_util | total_acc | mort_acc | pub_rec_bankruptcies | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| loan_amnt | 1.000000 | 0.168921 | 0.953929 | 0.336887 | 0.016636 | 0.198556 | -0.077779 | 0.328320 | 0.099911 | 0.223886 | 0.222315 | -0.106539 |

| int_rate | 0.168921 | 1.000000 | 0.162758 | -0.056771 | 0.079038 | 0.011649 | 0.060986 | -0.011280 | 0.293659 | -0.036404 | -0.082583 | 0.057450 |

| installment | 0.953929 | 0.162758 | 1.000000 | 0.330381 | 0.015786 | 0.188973 | -0.067892 | 0.316455 | 0.123915 | 0.202430 | 0.193694 | -0.098628 |

| annual_inc | 0.336887 | -0.056771 | 0.330381 | 1.000000 | -0.081685 | 0.136150 | -0.013720 | 0.299773 | 0.027871 | 0.193023 | 0.236320 | -0.050162 |

| dti | 0.016636 | 0.079038 | 0.015786 | -0.081685 | 1.000000 | 0.136181 | -0.017639 | 0.063571 | 0.088375 | 0.102128 | -0.025439 | -0.014558 |

| open_acc | 0.198556 | 0.011649 | 0.188973 | 0.136150 | 0.136181 | 1.000000 | -0.018392 | 0.221192 | -0.131420 | 0.680728 | 0.109205 | -0.027732 |

| pub_rec | -0.077779 | 0.060986 | -0.067892 | -0.013720 | -0.017639 | -0.018392 | 1.000000 | -0.101664 | -0.075910 | 0.019723 | 0.011552 | 0.699408 |

| revol_bal | 0.328320 | -0.011280 | 0.316455 | 0.299773 | 0.063571 | 0.221192 | -0.101664 | 1.000000 | 0.226346 | 0.191616 | 0.194925 | -0.124532 |

| revol_util | 0.099911 | 0.293659 | 0.123915 | 0.027871 | 0.088375 | -0.131420 | -0.075910 | 0.226346 | 1.000000 | -0.104273 | 0.007514 | -0.086751 |

| total_acc | 0.223886 | -0.036404 | 0.202430 | 0.193023 | 0.102128 | 0.680728 | 0.019723 | 0.191616 | -0.104273 | 1.000000 | 0.381072 | 0.042035 |

| mort_acc | 0.222315 | -0.082583 | 0.193694 | 0.236320 | -0.025439 | 0.109205 | 0.011552 | 0.194925 | 0.007514 | 0.381072 | 1.000000 | 0.027239 |

| pub_rec_bankruptcies | -0.106539 | 0.057450 | -0.098628 | -0.050162 | -0.014558 | -0.027732 | 0.699408 | -0.124532 | -0.086751 | 0.042035 | 0.027239 | 1.000000 |

The following is a strong visual of which features are most correlated to one another.

plt.figure(figsize=(12,8))

sns.heatmap(df.corr(),cmap='viridis',annot=True)<AxesSubplot:>

The installment amount is highly correlated to the loan amount, which makes sense.

df.columnsIndex(['loan_amnt', 'term', 'int_rate', 'installment', 'grade', 'sub_grade',

'emp_title', 'emp_length', 'home_ownership', 'annual_inc',

'verification_status', 'issue_d', 'loan_status', 'purpose', 'title',

'dti', 'earliest_cr_line', 'open_acc', 'pub_rec', 'revol_bal',

'revol_util', 'total_acc', 'initial_list_status', 'application_type',

'mort_acc', 'pub_rec_bankruptcies', 'address'],

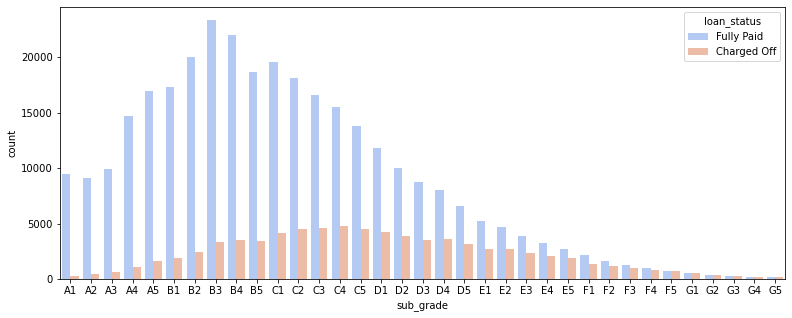

dtype='object')grade_order = list(df['grade'].sort_values().unique())subgrade_order = list(df['sub_grade'].sort_values().unique())The following shows the number of fully paid versus charged off accounts by grade.

We see that higher grades have more instances of paid off accounts than lower grades.

sns.countplot(x='grade',data=df,hue='loan_status',order=grade_order)<AxesSubplot:xlabel='grade', ylabel='count'>

The following is what looks to be a Poisson distribution of loans by subgrade.

plt.figure(figsize=(13,5))

sns.countplot(x='sub_grade',data=df,order=subgrade_order,palette='coolwarm')<AxesSubplot:xlabel='sub_grade', ylabel='count'>

We see in the following plot that when separated by the target variables, those with higher grades and subgrades have more instances of fully paid off loans, which is expected.

plt.figure(figsize=(13,5))

sns.countplot(x='sub_grade',data=df,order=subgrade_order,palette='coolwarm',hue='loan_status')<AxesSubplot:xlabel='sub_grade', ylabel='count'>

Those with F and G grades have closer to 50/50 odds of paying off their loans.

fg_df = df[(df['grade']=='F')|(df['grade']=='G')]

plt.figure(figsize=(13,5))

sns.countplot(x='sub_grade',data=fg_df,hue='loan_status',order=fg_df['sub_grade'].sort_values().unique(),palette='coolwarm')<AxesSubplot:xlabel='sub_grade', ylabel='count'>

Feature Engineering

Prepping data for our machine learning algorithm later.

def paid_charged(pc):

if pc == 'Fully Paid':

return 1

else:

return 0

df['loan_repaid'] = df['loan_status'].apply(lambda x: paid_charged(x))df[['loan_repaid','loan_status']]| loan_repaid | loan_status | |

|---|---|---|

| 0 | 1 | Fully Paid |

| 1 | 1 | Fully Paid |

| 2 | 1 | Fully Paid |

| 3 | 1 | Fully Paid |

| 4 | 0 | Charged Off |

| ... | ... | ... |

| 396025 | 1 | Fully Paid |

| 396026 | 1 | Fully Paid |

| 396027 | 1 | Fully Paid |

| 396028 | 1 | Fully Paid |

| 396029 | 1 | Fully Paid |

396030 rows × 2 columns

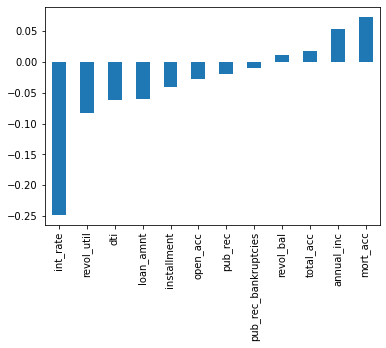

Interest rate has an inverse relationship to being repaid. Annual income and mortgage accounts have a stronger correlation to a loan being repaid.

df.corr()['loan_repaid'][:-1].sort_values().plot(kind='bar')<AxesSubplot:>

Missing Data

Missing data as percentages of the total data instances. The missing instances in Title, Revolving Utilization, and Public Record Bankruptcies are less than 1% and those instances can be deleted without impacting our dataset too much. The other three may need to have data imputed.

((df.isnull().sum())/(3960.30))loan_amnt 0.000000

term 0.000000

int_rate 0.000000

installment 0.000000

grade 0.000000

sub_grade 0.000000

emp_title 5.789208

emp_length 4.621115

home_ownership 0.000000

annual_inc 0.000000

verification_status 0.000000

issue_d 0.000000

loan_status 0.000000

purpose 0.000000

title 0.443148

dti 0.000000

earliest_cr_line 0.000000

open_acc 0.000000

pub_rec 0.000000

revol_bal 0.000000

revol_util 0.069692

total_acc 0.000000

initial_list_status 0.000000

application_type 0.000000

mort_acc 9.543469

pub_rec_bankruptcies 0.135091

address 0.000000

loan_repaid 0.000000

dtype: float64We will take a closer look at emp_title, emp_length, and mort_acc.

df['emp_title'].nunique()173105df['emp_title'].value_counts()Teacher 4389

Manager 4250

Registered Nurse 1856

RN 1846

Supervisor 1830

...

Warner Brothers 1

Liscened Practical Nirse 1

Crews Lake Middle School 1

Kaiser - Southern California Permanente 1

HIV Testing/Counseling Coordinator 1

Name: emp_title, Length: 173105, dtype: int64Employment Titles will be difficult to address effectively for our purposes. It would be hard to glean any useful and meaningful insights versus the cost to computing and time spent re-categorizing these titles. We will delete this column altogether.

df.drop('emp_title',axis=1,inplace=True)df['emp_length'].unique()array(['10+ years', '4 years', '< 1 year', '6 years', '9 years',

'2 years', '3 years', '8 years', '7 years', '5 years', '1 year',

nan], dtype=object)sorted(df['emp_length'].dropna().unique())['1 year',

'10+ years',

'2 years',

'3 years',

'4 years',

'5 years',

'6 years',

'7 years',

'8 years',

'9 years',

'< 1 year']order = ['< 1 year','1 year','2 years','3 years','4 years','5 years',

'6 years', '7 years', '8 years', '9 years','10+ years']plt.figure(figsize=(10,6))

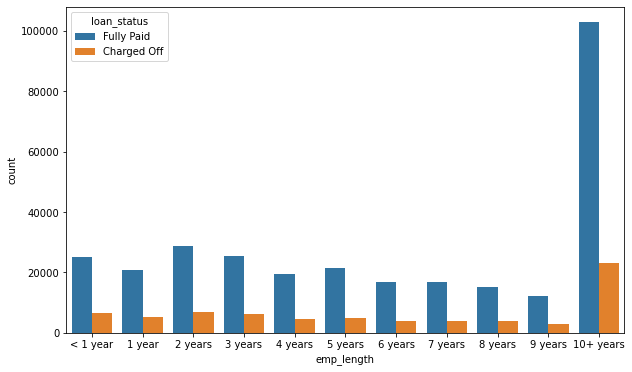

sns.countplot(x='emp_length',data=df,order=order)<AxesSubplot:xlabel='emp_length', ylabel='count'>

What is the relationship between our target variables and this feature?

plt.figure(figsize=(10,6))

sns.countplot(x='emp_length',data=df,order=order,hue='loan_status')<AxesSubplot:xlabel='emp_length', ylabel='count'>

df.columnsIndex(['loan_amnt', 'term', 'int_rate', 'installment', 'grade', 'sub_grade',

'emp_length', 'home_ownership', 'annual_inc', 'verification_status',

'issue_d', 'loan_status', 'purpose', 'title', 'dti', 'earliest_cr_line',

'open_acc', 'pub_rec', 'revol_bal', 'revol_util', 'total_acc',

'initial_list_status', 'application_type', 'mort_acc',

'pub_rec_bankruptcies', 'address', 'loan_repaid'],

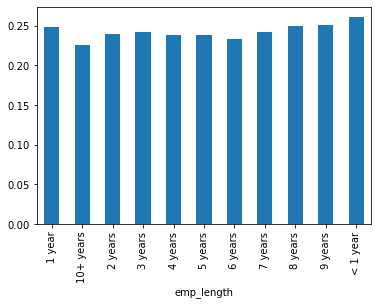

dtype='object')emp_co = df[df['loan_status']=="Charged Off"].groupby("emp_length").count()['loan_status']emp_fp = df[df['loan_status']=="Fully Paid"].groupby("emp_length").count()['loan_status']emp_len = emp_co/emp_fpemp_lenemp_length

1 year 0.248649

10+ years 0.225770

2 years 0.239560

3 years 0.242593

4 years 0.238213

5 years 0.237911

6 years 0.233341

7 years 0.241887

8 years 0.249625

9 years 0.250735

< 1 year 0.260830

Name: loan_status, dtype: float64emp_len.plot(kind='bar')<AxesSubplot:xlabel='emp_length'>

As a percentage of instances, the amount of charge off versus full repayment is consistent across employment lengths. We will drop this column as well.

df = df.drop('emp_length',axis=1)The title column is essentially the same as the purpose column. They are also both string columns.

df = df.drop('title',axis=1)df['mort_acc'].value_counts()0.0 139777

1.0 60416

2.0 49948

3.0 38049

4.0 27887

5.0 18194

6.0 11069

7.0 6052

8.0 3121

9.0 1656

10.0 865

11.0 479

12.0 264

13.0 146

14.0 107

15.0 61

16.0 37

17.0 22

18.0 18

19.0 15

20.0 13

24.0 10

22.0 7

21.0 4

25.0 4

27.0 3

23.0 2

32.0 2

26.0 2

31.0 2

30.0 1

28.0 1

34.0 1

Name: mort_acc, dtype: int64print("Correlation with the mort_acc column")

df.corr()['mort_acc'].sort_values()[:-1]Correlation with the mort_acc column

int_rate -0.082583

dti -0.025439

revol_util 0.007514

pub_rec 0.011552

pub_rec_bankruptcies 0.027239

loan_repaid 0.073111

open_acc 0.109205

installment 0.193694

revol_bal 0.194925

loan_amnt 0.222315

annual_inc 0.236320

total_acc 0.381072

Name: mort_acc, dtype: float64df.groupby('total_acc').mean()['mort_acc']total_acc

2.0 0.000000

3.0 0.052023

4.0 0.066743

5.0 0.103289

6.0 0.151293

...

124.0 1.000000

129.0 1.000000

135.0 3.000000

150.0 2.000000

151.0 0.000000

Name: mort_acc, Length: 118, dtype: float64tot_acc_avg = df.groupby('total_acc').mean()['mort_acc']tot_acc_avg[2.0]0.0The missing data will be imputed with the average value calculated by total accounts.

def fill_mort_acc(total_acc,mort_acc):

if np.isnan(mort_acc):

return tot_acc_avg[total_acc]

else:

return mort_accdf['mort_acc'] = df.apply(lambda x: fill_mort_acc(x['total_acc'],x['mort_acc']),axis=1)We have addresssed the most significant missing data points. We can drop other missing instances since it will not impact our overall dataset significantly.

df = df.dropna()We now have no more missing data points.

df.isnull().sum()loan_amnt 0

term 0

int_rate 0

installment 0

grade 0

sub_grade 0

home_ownership 0

annual_inc 0

verification_status 0

issue_d 0

loan_status 0

purpose 0

dti 0

earliest_cr_line 0

open_acc 0

pub_rec 0

revol_bal 0

revol_util 0

total_acc 0

initial_list_status 0

application_type 0

mort_acc 0

pub_rec_bankruptcies 0

address 0

loan_repaid 0

dtype: int64Non-numeric data features.

We can now address non-number data types in our set so we can run our algorithm.

list(df.select_dtypes(exclude='number').columns)['term',

'grade',

'sub_grade',

'home_ownership',

'verification_status',

'issue_d',

'loan_status',

'purpose',

'earliest_cr_line',

'initial_list_status',

'application_type',

'address']term feature

The 'term' column can be converted to a numerical column by taking the first portion of the inputs.

df['term'][0].split()['36', 'months']df['term'] = df['term'].apply(lambda x: int(x.split()[0]))df['term'].value_counts()36 301247

60 93972

Name: term, dtype: int64grade and sub_grade features

grade is part of sub_grade, so grade is dropped.

df = df.drop('grade',axis=1)sub_grade is converted to dummy variables and the original sub_grade column is deleted.

subs = pd.get_dummies(df['sub_grade'])df.drop('sub_grade',axis=1,inplace=True)df = pd.concat([df,subs],axis=1)verification_status, application_type, initial_list_status, purpose features

Again, we will convert to dummy variables.

ver_stat = pd.get_dummies(df['verification_status'])

app_type = pd.get_dummies(df['application_type'])

init_list_stat = pd.get_dummies(df['initial_list_status'])

purp = pd.get_dummies(df['purpose'])df = df.drop(['verification_status','application_type','initial_list_status','purpose'],axis=1)df = pd.concat([df,ver_stat,app_type,init_list_stat,purp],axis=1)list(df.select_dtypes(exclude='number').columns)['home_ownership', 'issue_d', 'loan_status', 'earliest_cr_line', 'address']home_ownership feature

df['home_ownership'].value_counts()MORTGAGE 198022

RENT 159395

OWN 37660

OTHER 110

NONE 29

ANY 3

Name: home_ownership, dtype: int64None and Any do not give us useful insights. They will be lumped together.

def home_own_type(ownership):

if ownership.lower() in ['none','any']:

return 'OTHER'

else:

return ownership

df['home_ownership'] = df['home_ownership'].apply(lambda x: home_own_type(x))home_own_type = pd.get_dummies(df['home_ownership'])df = df.drop('home_ownership',axis=1)

df = pd.concat([df,home_own_type],axis=1)address feature

We will extract zip codes from the address column and create dummy variables.

df['address'][0][-5:]'22690'df['zip_code'] = df['address'].apply(lambda x: x[-5:])zip_codes = pd.get_dummies(df['zip_code'])

df = df.drop('zip_code',axis=1)

df = pd.concat([df,zip_codes],axis=1)df = df.drop('address',axis=1)There are three columns remaining with non-numeric data types.

df.select_dtypes(exclude='number').columnsIndex(['issue_d', 'loan_status', 'earliest_cr_line'], dtype='object')issue_d feature

issue_d is the issue date, which is not a predicting feature for our target variables. We will drop this column.

df = df.drop('issue_d',axis=1)earliest_cr_line feature

We will extract the year from the earliest_cr_line feature and use that as a numeric feature.

df['earliest_cr_line'][0][-4:]'1990'df['earliest_cr_year'] = df['earliest_cr_line'].apply(lambda x: int(x[-4:]))

df = df.drop('earliest_cr_line',axis=1)df.select_dtypes(exclude='number').columnsIndex(['loan_status'], dtype='object')Working with our Model

Train Test Split

from sklearn.model_selection import train_test_splitWe have converted loan_repaid to numeric features, so we can drop loan_status, which is essentially a repeat of those values.

df = df.drop('loan_status',axis=1)X are the features, y are the target variables.

X = df.drop('loan_repaid',axis=1).values

y = df['loan_repaid'].valuesWe will take a portion of our full data, due to computing resources.

df = df.sample(frac=0.1,random_state=101)

print(len(df))39522X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.2, random_state=101)Normalizing Data

from sklearn.preprocessing import MinMaxScalerscaler = MinMaxScaler()X_train = scaler.fit_transform(X_train)

X_test = scaler.transform(X_test)Creating Model/Neural Network

from tensorflow.keras.models import Sequential

from tensorflow.keras.layers import Dense,Dropout

from tensorflow.keras.callbacks import EarlyStoppingX_train.shape(316175, 85)We will employ early stopping to reduce time.

early_stop = EarlyStopping(monitor='val_loss',mode='auto',verbose=1,patience=25)model = Sequential()

# Input layer with rectified linear unit activation function

model.add(Dense(78,activation='relu'))

model.add(Dropout(0.5))

# Hidden layers

model.add(Dense(39,activation='relu'))

model.add(Dropout(0.5))

model.add(Dense(19,activation='relu'))

model.add(Dropout(0.5))

# Output layer with sigmoid activation function

model.add(Dense(1,activation='sigmoid'))

# Model will use adam optimizer.

model.compile(loss='binary_crossentropy',optimizer='adam')model.fit(x=X_train,y=y_train,epochs=200,

validation_data=(X_test,y_test),

verbose=1,callbacks=[early_stop])Epoch 1/200

9881/9881 [==============================] - 9s 954us/step - loss: 0.2907 - val_loss: 0.2663

Epoch 2/200

9881/9881 [==============================] - 9s 942us/step - loss: 0.2669 - val_loss: 0.2648

Epoch 3/200

9881/9881 [==============================] - 10s 962us/step - loss: 0.2659 - val_loss: 0.2640

Epoch 4/200

9881/9881 [==============================] - 9s 952us/step - loss: 0.2654 - val_loss: 0.2639

Epoch 5/200

9881/9881 [==============================] - 9s 941us/step - loss: 0.2651 - val_loss: 0.2632

Epoch 6/200

9881/9881 [==============================] - 9s 953us/step - loss: 0.2646 - val_loss: 0.2635

Epoch 7/200

9881/9881 [==============================] - 9s 952us/step - loss: 0.2644 - val_loss: 0.2625

Epoch 8/200

9881/9881 [==============================] - 10s 966us/step - loss: 0.2647 - val_loss: 0.2631

Epoch 9/200

9881/9881 [==============================] - 10s 967us/step - loss: 0.2643 - val_loss: 0.2628

Epoch 10/200

9881/9881 [==============================] - 9s 954us/step - loss: 0.2642 - val_loss: 0.2633

Epoch 11/200

9881/9881 [==============================] - 10s 970us/step - loss: 0.2642 - val_loss: 0.2634

Epoch 12/200

9881/9881 [==============================] - 10s 966us/step - loss: 0.2643 - val_loss: 0.2630

Epoch 13/200

9881/9881 [==============================] - 10s 1ms/step - loss: 0.2643 - val_loss: 0.2622

Epoch 14/200

9881/9881 [==============================] - 10s 1ms/step - loss: 0.2645 - val_loss: 0.2630

Epoch 15/200

9881/9881 [==============================] - 10s 964us/step - loss: 0.2642 - val_loss: 0.2626

Epoch 16/200

9881/9881 [==============================] - 9s 961us/step - loss: 0.2641 - val_loss: 0.2627

Epoch 17/200

9881/9881 [==============================] - 9s 954us/step - loss: 0.2638 - val_loss: 0.2634

Epoch 18/200

9881/9881 [==============================] - 10s 969us/step - loss: 0.2640 - val_loss: 0.2631

Epoch 19/200

9881/9881 [==============================] - 10s 962us/step - loss: 0.2638 - val_loss: 0.2620

Epoch 20/200

9881/9881 [==============================] - 10s 984us/step - loss: 0.2639 - val_loss: 0.2622

Epoch 21/200

9881/9881 [==============================] - 10s 973us/step - loss: 0.2635 - val_loss: 0.2623

Epoch 22/200

9881/9881 [==============================] - 9s 960us/step - loss: 0.2635 - val_loss: 0.2628

Epoch 23/200

9881/9881 [==============================] - 10s 970us/step - loss: 0.2633 - val_loss: 0.2624

Epoch 24/200

9881/9881 [==============================] - 10s 966us/step - loss: 0.2638 - val_loss: 0.2636

Epoch 25/200

9881/9881 [==============================] - 9s 959us/step - loss: 0.2637 - val_loss: 0.2629

Epoch 26/200

9881/9881 [==============================] - 10s 962us/step - loss: 0.2637 - val_loss: 0.2633

Epoch 27/200

9881/9881 [==============================] - 10s 971us/step - loss: 0.2637 - val_loss: 0.2647

Epoch 28/200

9881/9881 [==============================] - 10s 975us/step - loss: 0.2635 - val_loss: 0.2630

Epoch 29/200

9881/9881 [==============================] - 10s 967us/step - loss: 0.2631 - val_loss: 0.2623

Epoch 30/200

9881/9881 [==============================] - 9s 957us/step - loss: 0.2632 - val_loss: 0.2645

Epoch 31/200

9881/9881 [==============================] - 10s 963us/step - loss: 0.2632 - val_loss: 0.2620

Epoch 32/200

9881/9881 [==============================] - 10s 978us/step - loss: 0.2631 - val_loss: 0.2637

Epoch 33/200

9881/9881 [==============================] - 9s 959us/step - loss: 0.2633 - val_loss: 0.2630

Epoch 34/200

9881/9881 [==============================] - 10s 974us/step - loss: 0.2633 - val_loss: 0.2636

Epoch 35/200

9881/9881 [==============================] - 10s 965us/step - loss: 0.2636 - val_loss: 0.2622

Epoch 36/200

9881/9881 [==============================] - 10s 970us/step - loss: 0.2628 - val_loss: 0.2619

Epoch 37/200

9881/9881 [==============================] - 9s 961us/step - loss: 0.2627 - val_loss: 0.2629

Epoch 38/200

9881/9881 [==============================] - 10s 966us/step - loss: 0.2632 - val_loss: 0.2628

Epoch 39/200

9881/9881 [==============================] - 10s 967us/step - loss: 0.2629 - val_loss: 0.2618

Epoch 40/200

9881/9881 [==============================] - 9s 960us/step - loss: 0.2633 - val_loss: 0.2627

Epoch 41/200

9881/9881 [==============================] - 10s 962us/step - loss: 0.2630 - val_loss: 0.2625

Epoch 42/200

9881/9881 [==============================] - 9s 956us/step - loss: 0.2636 - val_loss: 0.2621

Epoch 43/200

9881/9881 [==============================] - 10s 972us/step - loss: 0.2634 - val_loss: 0.2627

Epoch 44/200

9881/9881 [==============================] - 10s 965us/step - loss: 0.2631 - val_loss: 0.2628

Epoch 45/200

9881/9881 [==============================] - 10s 964us/step - loss: 0.2632 - val_loss: 0.2622

Epoch 46/200

9881/9881 [==============================] - 10s 962us/step - loss: 0.2631 - val_loss: 0.2638

Epoch 47/200

9881/9881 [==============================] - 9s 960us/step - loss: 0.2634 - val_loss: 0.2624

Epoch 48/200

9881/9881 [==============================] - 9s 956us/step - loss: 0.2626 - val_loss: 0.2623

Epoch 49/200

9881/9881 [==============================] - 10s 968us/step - loss: 0.2632 - val_loss: 0.2627

Epoch 50/200

9881/9881 [==============================] - 10s 962us/step - loss: 0.2628 - val_loss: 0.2640

Epoch 51/200

9881/9881 [==============================] - 10s 968us/step - loss: 0.2627 - val_loss: 0.2632

Epoch 52/200

9881/9881 [==============================] - 9s 961us/step - loss: 0.2628 - val_loss: 0.2624

Epoch 53/200

9881/9881 [==============================] - 10s 967us/step - loss: 0.2631 - val_loss: 0.2618

Epoch 54/200

9881/9881 [==============================] - 9s 954us/step - loss: 0.2628 - val_loss: 0.2621

Epoch 55/200

9881/9881 [==============================] - 10s 961us/step - loss: 0.2629 - val_loss: 0.2644

Epoch 56/200

9881/9881 [==============================] - 10s 966us/step - loss: 0.2636 - val_loss: 0.2630

Epoch 57/200

9881/9881 [==============================] - 10s 966us/step - loss: 0.2635 - val_loss: 0.2623

Epoch 58/200

9881/9881 [==============================] - 9s 957us/step - loss: 0.2630 - val_loss: 0.2624

Epoch 59/200

9881/9881 [==============================] - 10s 988us/step - loss: 0.2626 - val_loss: 0.2639

Epoch 60/200

9881/9881 [==============================] - 10s 974us/step - loss: 0.2628 - val_loss: 0.2636

Epoch 61/200

9881/9881 [==============================] - 10s 965us/step - loss: 0.2631 - val_loss: 0.2628

Epoch 62/200

9881/9881 [==============================] - 10s 963us/step - loss: 0.2629 - val_loss: 0.2636

Epoch 63/200

9881/9881 [==============================] - 10s 1ms/step - loss: 0.2635 - val_loss: 0.2626

Epoch 64/200

9881/9881 [==============================] - 10s 1ms/step - loss: 0.2630 - val_loss: 0.2624

Epoch 00064: early stopping

<tensorflow.python.keras.callbacks.History at 0x7fb361785ba8>Saving this model for future use.

from tensorflow.keras.models import load_modelmodel.save('lending_club_model.h5')Evaluating Model Performance

model_loss = pd.DataFrame(model.history.history)

model_loss.plot()<AxesSubplot:>

predictions = model.predict_classes(X_test)from sklearn.metrics import classification_report,confusion_matrixprint(confusion_matrix(y_test,predictions))

print(classification_report(y_test,predictions))[[ 6831 8827]

[ 90 63296]]

precision recall f1-score support

0 0.99 0.44 0.61 15658

1 0.88 1.00 0.93 63386

accuracy 0.89 79044

macro avg 0.93 0.72 0.77 79044

weighted avg 0.90 0.89 0.87 79044Predicting One Input

import random

random.seed(101)

random_ind = random.randint(0,len(df))

new_customer = df.drop('loan_repaid',axis=1).iloc[random_ind]

new_customerloan_amnt 25000.00

term 36.00

int_rate 7.90

installment 782.26

annual_inc 62000.00

...

48052 0.00

70466 1.00

86630 0.00

93700 0.00

earliest_cr_year 1991.00

Name: 385487, Length: 85, dtype: float64model.predict_classes(new_customer.values.reshape(1,85))array([[1]], dtype=int32)It appears this person is likely to repay their loan.

df.iloc[random_ind]['loan_repaid']1.0They did in fact repay their loan.